Burn injury settlements vary widely, from a few thousand dollars for minor burns to millions for severe cases. Understanding what determines these amounts is crucial. Settlement values depend on factors like:

For fair compensation, keep detailed records of medical expenses, lost wages, and emotional impacts. Legal representation can significantly increase settlement outcomes.

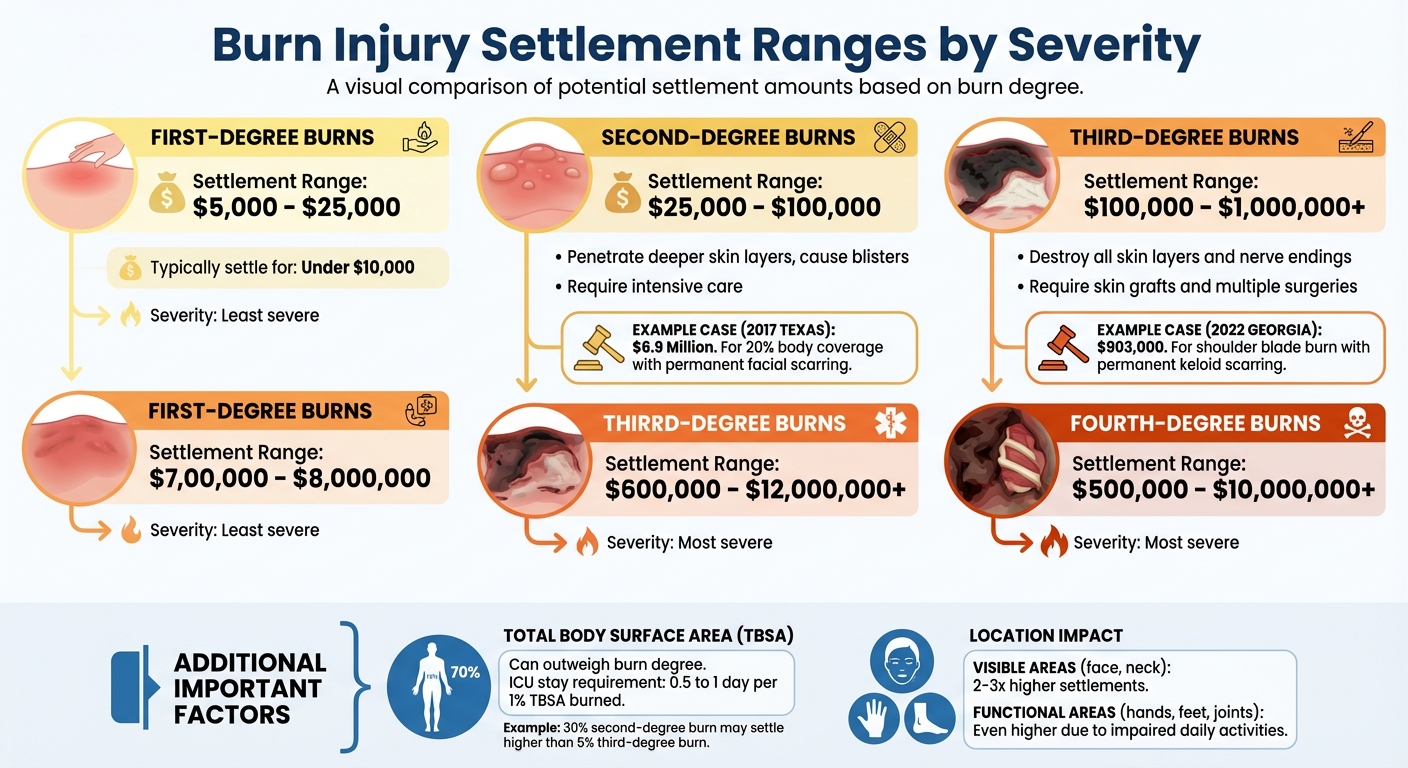

Burn Injury Settlement Ranges by Severity and Degree

The depth of tissue damage plays a key role in determining the value of a burn injury claim. Burn classifications - ranging from first-degree to fourth-degree - directly influence the level of medical care required and the long-term physical effects. For instance, settlements for first-degree burns can range from $5,000 to $25,000, while fourth-degree burns may result in payouts between $500,000 and $10,000,000 or more.

In some cases, the Total Body Surface Area (TBSA) burned can outweigh the burn degree in determining settlement amounts. For example, a second-degree burn covering 30% of the body might result in a higher payout than a third-degree burn affecting just 5% of the body. Larger burns often require extended ICU stays - about 0.5 to 1 day for each 1% of TBSA burned - and carry greater risks of complications like infections. A notable case in 2017 saw a Texas jury award $6.9 million to a plaintiff with second-degree burns over 20% of his body caused by an improperly installed gas valve. Permanent facial scarring played a significant role in this settlement.

Burn location also plays a major role in determining compensation.

The location of a burn can significantly influence settlement amounts. Burns on highly visible areas like the face or neck often result in payouts 2 to 3 times higher than similar burns on less visible areas. This reflects both the physical and emotional toll of such injuries.

Burns on functional areas like hands, feet, or joints can lead to even higher settlements. Injuries in these regions often impair daily activities and work capabilities. According to the American Burn Association, these burns frequently require treatment in specialized facilities, which increases medical costs. Additionally, scarring around joints can lead to contractures, limiting movement and necessitating reconstructive surgery and therapy. In one 2022 case, a Georgia jury awarded $903,000 to a plaintiff who suffered a third-degree burn to his shoulder blade during physical therapy, resulting in permanent keloid scarring.

Medical expenses are a cornerstone in determining burn injury settlements. The severity of the burn directly impacts treatment costs, with average burn-related hospital stays costing around $24,000. However, in severe cases, hospitalization expenses can range from $10,000 to over $125,000, depending on the injury's depth and the care required. These initial costs lay the groundwork for evaluating both immediate and long-term medical needs.

Severe burns often demand urgent emergency room care followed by admission to specialized burn units, which significantly increases expenses. For example, nearly 29% of burn cases involve skin grafts, each costing over $17,000. Additionally, infections - a complication in roughly 35% of severe burn cases - can add an extra $120,000 to the overall medical bill.

For minor burns requiring outpatient care, costs typically range between $5,000 and $15,000. On the other hand, catastrophic cases involving extended ICU stays, multiple skin grafts, and reconstructive surgeries can push medical expenses beyond $1,000,000. These figures play a critical role in determining settlement values.

Estimating future medical requirements is essential for a fair settlement, particularly in severe cases. Victims may need ongoing care for 5 to 10 years or more, including scar revision surgeries, physical therapy, and psychological support. To address this, life care plans - created by certified specialists - offer detailed projections of future costs. These plans can enhance settlement negotiations by 30% to 50%.

"Life care plans prepared by certified specialists provide crucial documentation of future needs and substantially strengthen settlement negotiations, often increasing final compensation by 30-50%." - Eric Richman Law Research Study

Key factors influencing total medical costs include the burn's extent (percentage of body surface area), tissue damage depth, and the presence of inhalation injuries. Settlements for younger victims are often higher, as their lifetime medical needs may span 60 to 70+ years. Additional expenses, such as home modifications for accessibility - like wheelchair ramps or specialized bathing facilities - can add $50,000 to $300,000 to the total claim.

Burn injuries don’t just come with mounting medical bills - they can also leave a lasting mark on your financial stability by affecting your ability to earn a living. Settlements for such injuries often factor in lost wages and diminished earning capacity, covering both the income you’ve already lost and the future earnings you may never regain due to permanent limitations.

If your injury keeps you from working, calculating lost wages involves summing up all income missed from the date of the injury until you either return to work or reach maximum medical improvement. This includes your base salary, commissions, and bonuses. For example, workers’ compensation claims for burn injuries typically provide an average of $13,277 in indemnity benefits (wage loss).

If you’re entirely unable to work, Temporary Total Disability (TTD) benefits generally cover two-thirds of your pre-injury weekly wage. On the other hand, if you return to work at a reduced capacity, Temporary Partial Disability (TPD) benefits cover two-thirds of the wage difference. On average, workers’ compensation settlements hover around $63,000. However, personal injury lawsuits may allow you to recover 100% of your lost wages.

To strengthen your claim, keep detailed records like medical documentation, pay stubs, and tax returns that verify your lost income, including bonuses and commissions. While immediate wage losses reflect short-term setbacks, the broader economic impact often comes from long-term earning potential.

For those with permanent disabilities caused by burns, the financial consequences extend far beyond immediate income loss. Whether it’s mobility issues from contractures or severe facial scarring that affects professionals in appearance-critical roles, settlements must address how these injuries reduce your earning potential over a lifetime. This involves comparing your expected income before the injury to what you can realistically earn now given your limitations.

Younger individuals often receive higher settlements because their projected income loss spans decades - sometimes 60 to 70 years. Vocational experts play a key role in these cases, evaluating your pre- and post-injury earning potential. If you’re forced to switch to a lower-paying career due to your injuries, settlements may compensate for the gap between your previous high-skill job and your new role, as well as the lost opportunities in your original career path.

To support these claims, gather documentation like records of promotions, performance reviews, and industry salary data to show what your future earnings might have been. Settlements may also include compensation for non-salary benefits like 401(k) contributions, stock options, and employer-paid insurance premiums.

When pursuing a burn injury claim, proving liability is just as important as documenting medical and financial losses. Even with severe injuries and mounting medical bills, a settlement hinges on showing that someone else is legally responsible. To establish negligence, you need to prove four key elements: the defendant owed you a duty of care, they breached that duty, the breach directly caused your burn injury, and you suffered measurable harm as a result. Without these elements, the claim won't stand - no matter how devastating the injuries.

Building a strong negligence case requires solid evidence. Medical records play a pivotal role by linking the incident to your injuries, outlining the extent of tissue damage, and detailing the severity of burns. Accident reports from police or fire departments offer objective accounts of what occurred at the scene. If a defective product caused the burns, preserving the item for expert analysis can help establish manufacturer liability.

Eyewitness accounts are also invaluable. Testimonies from bystanders, coworkers, or first responders can clarify the circumstances of the accident. For example, a witness might confirm that a landlord ignored repeated complaints about faulty wiring, which eventually led to a fire. Expert testimony adds further weight to your case. Medical professionals can explain the long-term physical and psychological effects of your burns, while safety specialists or fire investigators can verify whether negligence - like a company ignoring safety protocols - directly caused the injury. Expert assessments detailing long-term care needs can further demonstrate the impact of the injuries.

"A 'duty of care' is the obligation to avoid causing harm to another person, either by action or inaction." - Enjuris

Photographic evidence is another crucial element. Document your burns with photos taken immediately after the incident and throughout the healing process. These visuals can prevent insurance companies from downplaying the severity of your injuries. Comprehensive evidence not only strengthens your case for liability but also supports a claim for higher compensation. If gross negligence is involved, it can even open the door to punitive damages, as discussed below.

After proving standard negligence, demonstrating gross negligence can significantly increase the potential settlement. Gross negligence involves behavior that goes beyond carelessness to include extreme recklessness or intentional harm. In such cases, you may qualify for punitive damages in addition to standard compensation. These damages aim to punish the responsible party and discourage similar actions in the future, often leading to much higher settlements. For instance, a manufacturer knowingly selling a flammable product without proper safety testing exemplifies the kind of conduct that warrants punitive damages.

The potential for punitive damages often prompts corporations or wealthy defendants to settle quickly and for larger amounts, avoiding the risk of a costly jury verdict. For example, a manufacturer of a dangerously flammable skirt agreed to a settlement of nearly $4,000,000 after a plaintiff sustained third-degree burns and permanent scarring on her torso. In another case, a gas station owner who overfilled a propane tank - resulting in an explosion during a barbecue - settled for $970,000 after the victim suffered second- and third-degree burns. These cases highlight how proving gross negligence can turn a moderate claim into a substantial recovery.

Insurance policy limits define the maximum amount an insurer will pay for a single accident or injury claim. In severe burn cases, damages often exceed these limits, leaving victims struggling to cover medical bills, lost income, and pain and suffering. For example, California's minimum auto insurance coverage - $15,000 per person and $30,000 per accident - falls short when you consider that the average hospitalization cost for serious auto injuries exceeds $57,000. For burn victims, hospital expenses can range from $10,000 to over $125,000, depending on the severity.

The type of insurance policy plays a critical role in these situations. A standard commercial policy usually offers $1,000,000 or more in coverage for moderate to severe burn claims. Umbrella policies provide an additional layer of protection, offering between $1,000,000 and $5,000,000 in secondary coverage once the primary policy is exhausted. These policies are relatively affordable, costing around $150 to $300 annually for every $1 million in extra coverage. However, when damages exceed all available insurance, the at-fault party becomes personally responsible for the "excess judgment." This can lead to the liquidation of personal assets, such as bank accounts, vehicles, investments, or real estate, to satisfy the remaining amount. These challenges highlight the importance of exploring other ways to secure full compensation.

When damages surpass insurance policy limits, alternative strategies can help secure additional compensation. One key approach is identifying all liable parties. For instance, a single burn incident might involve multiple at-fault entities, such as a negligent driver, a vehicle manufacturer (in cases of product defects), or a government agency responsible for unsafe road conditions. Each of these parties may have separate insurance policies, opening up multiple sources of compensation. If the at-fault party was working during the accident, their employer's commercial insurance policy might also come into play under vicarious liability, often offering much higher coverage limits.

Another option is filing a claim under your own Underinsured Motorist (UIM) coverage. If the at-fault driver’s insurance isn’t enough to cover your damages, UIM coverage can help bridge the gap. In California, about 70% of insured drivers carry some form of UIM coverage, making it a valuable resource in cases of insufficient coverage. Additionally, if an insurer unreasonably refuses to settle within policy limits despite clear liability, they could be held responsible for the entire judgment through a "bad faith" claim.

Legal representation is another factor that can significantly impact settlements. Claimants who work with attorneys tend to receive settlements that are, on average, 3.5 times larger than those who handle claims on their own. This underscores the importance of professional legal guidance when navigating the complexities of insurance policy limits.

Fair burn injury settlements hinge on several factors, including the severity and location of your burns, medical costs, future care needs, lost earning potential, and the strength of your liability case. Understanding these elements is key to securing compensation that addresses your lifelong needs.

Keep detailed records of your treatments, expenses, and daily challenges to support both economic and non-economic damages. Document every medical procedure, out-of-pocket cost, and missed workday. Maintaining a daily journal of your pain levels, mobility issues, and emotional struggles can provide powerful evidence, making it harder for insurance companies to downplay your claim.

This comprehensive documentation becomes the foundation of a strong case, which skilled legal representation can further strengthen. An experienced legal team collaborates with medical professionals, life care planners, and vocational experts to build a case that fully accounts for the impact of your injuries.

Because burn injury claims are complex and involve many factors, True North Injury Law offers a free consultation to evaluate your case and explain your options. Their team understands the life-altering effects of burn injuries and works to secure compensation that addresses not only immediate costs but also long-term medical, financial, and emotional needs. With solid evidence and expert legal support, you can pursue a settlement that truly accounts for your ongoing challenges.

The timeline for resolving a burn injury case can vary widely and often depends on several key factors: the complexity of the case, the severity of the burns, and whether the case is settled through negotiation or proceeds to trial. For straightforward cases where liability is clear, the process may wrap up within 6 to 12 months. However, more complicated cases - especially those involving disputes over evidence or liability - can take 2 to 3 years or even longer if they end up in court. Progress often hinges on how quickly evidence is gathered, liability is established, and negotiations advance.

Key details in a burn injury case revolve around how and where the injury happened. Was it the result of a workplace incident? Did a defective product play a role? Or was it caused by someone’s negligence? These factors are critical in establishing liability and shaping the direction of the case.

If the at-fault party's insurance policy doesn't provide enough coverage, it might not fully address all the damages. In these situations, the injured party may need to consider other legal avenues, such as filing a lawsuit against the at-fault individual, to seek additional compensation.